A surge in new UK hotels and refurbishments is on the way in the wake of the recession and ahead of the Olympics, reveals David Churchill

HOTEL PROJECTS DELAYED during the downturn are now coming to fruition, and a general recovery in business travel has helped fuel a surge in planned openings and refurbishments in the UK. This is a boom, moreover, that is outpacing the rest of Europe. According to hotel consultants STR Global, the UK will account for nearly one-third of the total number of new hotel rooms across Europe coming on stream in 2012.

Elizabeth Randall, managing director of STR Global, says: "We expect the UK to see 13,271 rooms opening next year as part of a total of 45,532 in Europe as a whole, with some 7,799 rooms opening in the first six months of the year."

Over the next year STR says that major regional cities, such as Birmingham, Manchester and Glasgow, are expected to open more rooms than capitals such as Moscow, which currently charges some of the highest rates in the world for hotel accommodation.

London is going through a boom in luxury hotels, with an estimated £1 billion being spent on new upscale properties in the run-up to the Olympics. (See 'Suite Dreams', BBT March/April). Moreover, according to the hospitality division of PricewaterhouseCoopers (PwC), there will be an increase of more than 10 per cent in London's total hotel room-stock between 2010 and 2012 - something PwC describes as "an unprecedented supply shock" to the system.

Jonathan Langston, managing director of TRI Hospitality Consulting, says that his company's monitoring of the UK hotels market continues to show that while the London sector has recovered in terms of occupancy and rates, the position in the regions is significantly weaker. "It is obviously a mixed picture to some degree, but there are some regional cities - such as Leeds - where the corporate demand has been hit by the recession and extra room supply has only added to the problem."

Nigel Turner, CWT's director of programme management, UK and Ireland, agrees there appears to be a divide between London's stronger hotel market and the rest of the country. "For this reason London hotels are becoming reluctant to commit any further rooms at negotiated rates," he says. "But we have found [hotel] suppliers more open to negotiation in cities such as Liverpool, Leeds, Birmingham and Glasgow."

Travel buyers do have more clout outside London, agrees Johan Persson, vice president for account management at Portman Travel. "It is true to say that buyers are stronger in the regions, because the perception of demand being weaker outside of the capital remains," he says.

Yet this regional weakness is no real deterrent to the major hotel chains who believe there is still plenty of potential in the overall UK market - not just in London - to increase their share of business. Consultants KPMG, for example, said in a 2010 report concerning the UK hotels market that even with the inroads made by the branded chains during the recession - when smaller, independent hotels were more likely to go under - "the proportion of branded hotels in the UK, whilst growing, remains relatively low at about 25 per cent, and the market as a whole is highly fragmented".

New Whitbread chief executive officer, Andy Harrison (formerly head of easyJet) reinforced this point after announcing a near-11 per cent hike in sales at Whitbread's Premier Inn chain in the full-year results to March 3, 2011.

"We're already winning market share from the independent sector," he said. Yet even though Premier Inn is Britain's biggest hotel chain, with 585 hotels and 42,654 rooms, Whitbread estimates that it only has 6 per cent of the total UK market for hotel accommodation.

The low-cost market, however, is where most of the sector's growth is planned as the budget hoteliers chase volume rather than rates. Both Premier Inn and its smaller rival, Travelodge, have set out ambitious growth targets: Premier Inn with 4,000 extra rooms this year and about 65,000 more over the next five years; Travelodge, which has 452 hotels and 30,988 rooms, is aiming for 1,100 properties and 100,000 rooms by 2025.

Both chains are also developing reduced-scale budget hotels to capitalise on smaller properties, which have become available in the wake of the recession, such as pubs, cinemas and office buildings. Travelodge, for example, found when it acquired 52 Innkeeper's Lodge budget hotels from Mitchells & Butlers last year, it could run the 20-room properties as profitably as its bigger hotels of at least 40 rooms. Now it is actively targeting these opportunities.

Premier Inn is also developing smaller hotels in suitable sites, such as in mixed-use developments and over high street stores, installing automatic check-in facilities to maximise the available space.

But the big hotel groups also have ambitious growth plans. InterContinental Hotels Group, the world's biggest hotelier in terms of rooms, already has 264 UK hotels with another 33 in its UK pipeline over the next couple of years, across its spread of brands. These include a new InterContinental at Westminster next year, a Crowne Plaza opening this summer at Colchester Five Lakes in Essex, seven Hotel Indigo properties (including in Birmingham and Edinburgh), two Staybridge Suites and 22 Holiday Inns or Holiday Inn Expresses.

Hilton Worldwide has plans to grow its mid-market Doubletree by Hilton brand in the UK, with another four hotels set to open over the next 12 months in addition to the current eight.

Rob Palleschi, global head of the Doubletree brand at Hilton, says: "We have two hotels in London at present but could have up to six." He reveals the group is also "looking at opportunities in Manchester, Glasgow, Newcastle and Brighton". Eventually, 25 UK Doubletrees are envisaged.

Accor, one of Europe's biggest hotels groups, has also been active in the UK. Last April, for example, the 331-room St Ermin's hotel in Westminster re-opened after a £30 million facelift as the first of Accor's new upscale brand, MGallery, in the UK. This year, moreover, Accor has added 13 mid-market hotels to its UK portfolio - including the Mercure London Paddington in the spring - as part of plans to increase its UK presence from 145 hotels to about 300 by 2015.

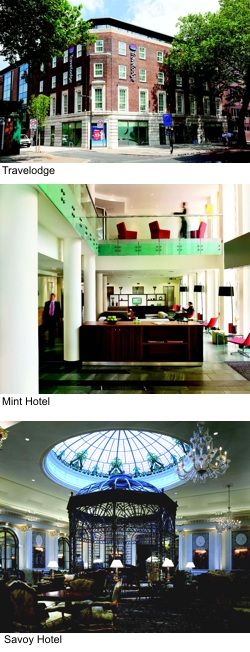

The major chains are not just focused on openings - refurbishment of existing properties is also seen as vital in maintaining their market position. The Thistle hotels group is in the middle of £100m, two-year refurbishment of its 33 UK hotels. The Thistle Portland hotel in Manchester, for example, has undergone an eight-month revamp, which saw improved air-conditioning and a new look for its 204 rooms.

Birmingham's Mint Hotel has also recently been refurbished to celebrate it 10th anniversary in the UK's second city. Mint was the name adopted late last year by the owners of the former City Inn group who felt many customers mistook the original name for a budget brand rather than a midscale property.

But Mint's UK development plans appear to have been put on hold while ownership of the group is decided. Earlier this year Lloyds Banking Group, co-owner with the Orr family who created the seven-strong group, put the business up for sale (Lloyds inherited its stake via the rescue deal for HBOS in 2008).

Potential buyers are said to include US private equity firm Blackstone Group, the majority owner of Hilton.

Other smaller UK hotel groups are also in a state of flux, which could affect ownership and future plans. Marylebone Warwick Balfour (MWB), for example, is considering selling some of its Malmaison or Hotel du Vin properties to reduce debt, while administrators to the collapsed von Essen Hotels holding company have put its 26 UK country house properties up for sale.

Yet although the growth and improvement of UK hotel stock is obviously a benefit for most travellers, new hotels do not necessarily make corporate clients willing to pay more. "I don't know of any travel manager or buyer who would pick a new hotel just because it is new," points out Margaret Bowler, director of global hotel relations at HRG. "It is still very much the case that price, value and location are the important factors."

Portman's Persson agrees that buyers are only interested in a new hotel or refurbishment "if it translates into a better deal for them", as "it may be approached in order to gain leverage with a current supplier".

On the Olympic way...

From the end of August travellers using Heathrow T5 will be able to check-in to a new 350-room Hilton just a mile from the terminal building. The property has meetings and event space for 1,170 delegates.

Following Travelodge's acquisition of the existing four-star Mercure airport hotel at Gatwick, there are plans for a substantial refurbishment to expand the number of rooms from 257 to 400. The hotel will remain open while the work takes place.

Also due to re-open in August after being acquired by Hallmark Hotels is the refurbished Aerodrome Hotel at Croydon.

Meanwhile, Rezidor is set to open its fifth UK airport hotel in late autumn, with a 216-room property under the Radisson Blu brand 800m from East Midlands Airport.

Other openings include The Dorchester's sibling luxury hotel, 45 Park Lane, due to open in September, and a 203-room Jurys Inn in Newcastle. Next spring, Birmingham will gain a 174-room four-star Hotel La Tour as part of the new City Park Gate development.

Among the Olympic-inspired openings due early next year is a 235-room Park Inn, located on the Olympic Way leading to Wembley Stadium (marking the 1948 Games held there).

LOOKING AHEAD...

Post-Olympics, there are plenty of projects getting underway. In addition to the ambitious expansion planned in the budget sector, with Premier Inn adding around 65,000 more rooms over the next five years and Travelodge's target of 1,100 properties by 2025, there are a number of specific projects being discussed. Liverpool is set to gain its first five-star hotel as developers are currently in negotiations with major chains to adopt one of their upscale brands, and there has been speculation over a number of different sites.

London will expand its luxury portfolio: a new Four Seasons in the City, close to Liverpool Street Station, is due to open in 2013, and Firmdale Hotels has plans for a 90-room property - as yet unnamed - in a new development at Ham Yard, in the heart of London's Soho. Also headed for London in 2013 is a 223-room Park Inn from Rezidor at the ExCel Exhibition centre in Docklands, adding much needed rooms and meeting space.

ALREADY CHECKED IN...

When the Savoy Hotel re-opened late last year after a £200m facelift it marked the start of a surge in new luxury accommodation in London that is still underway.

The Savoy's return was soon followed by the Four Seasons in Park Lane, coming back on-stream with the addition of a new floor of suites, along with the transformation in the spring of the former railway hotel at St Pancras under the Renaissance banner, one of the Marriott brands. But it was not all one-way traffic for Marriott: this June it gave up the management contract to operate the London Chancery Court Hotel under the Renaissance brand.

Another notable addition to the London luxury scene this year is Starwood's first boutique W hotel in the UK, in London's Leicester Square.

Outside the capital, InterContinental Hotels Group opened a 95-room Hotel Indigo in Glasgow, its third such property in the UK. In April, budget brand Days Inn opened in Liverpool, while in May, Ireland's Dalata group launched its first hotel in the UK with the 216-room Maldron Hotel in Cardiff, the first of a planned UK expansion across major cities.